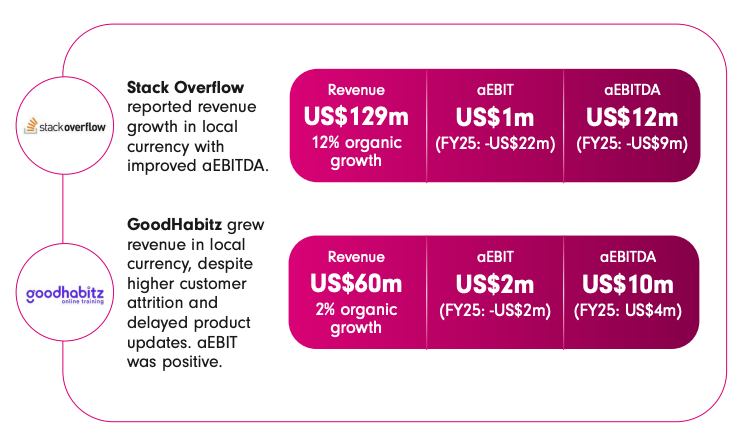

A couple years ago I asked How’s business at Stack Overflow? Prosus, the current owner of Stack Overflow, issued an annual report for the year than ended in March, 2026. The graphic featuring Stack Overflow puts a positive spin on the situation:

I had to look up GoodHabitz. It’s an online training company that Prosus bought around the same time as Stack Overflow. It was clearly a poor investment since it’s usually linked to Stack Overflow in the annual reports in the descriptions of “impairment losses on goodwill”. More on that in a bit.

“12% organic growth” in revenue sounds good. “Organic” just means the growth didn’t come from buying another company. It’s growing the business by finding more customers, charging customers more or both. 12% is marginally better than the default investment, but nowhere close to the 20% or more growth the purchase price assumed.

Next we have “a EBIT” and"aEBITDA". These stand for:

- adjusted earnings before interest and taxes (aEBIT)

- adjusted earnings before interest, taxes, and amortization (aEBITA)

Neither metric is as useful for evaluating an investment as simple gross earnings (revenue - cost of goods and services) or net earnings (revenue - all expenses). EBITA is especially nonsensical when it comes to a business, such as Stack Overflow, that create intangible assets, specifically software, and amortize the cost over time. Presumably Stack Overflow released new features in hopes of growing their revenue. Rather than accounting for that expense all at once, it spread the cost over the (theoretical) life of the feature.

EBIT, which just removes interest and taxes, is a slightly more honest measure of profitability. Businesses still need to pay taxes and interest on debt, but those expenses can be somewhat orthogonal to how well the business is managed. Managers prefer these not-quite-earnings measurements because they tend to inflate the perceived profitability of an operation. Even so, Stack Overflow has only just become profitable by the overly-generous metric.

Searching the rest of the annual report for “Stack Overflow”, much of the discussion is about “impairment of goodwill”. When one company buys another, the various assets that were purchased are recorded in the balance sheet. This is sometimes called the “book value”. But usually a company is purchased for a price in excess of the book value. That excess is recorded as “goodwill” and accounts for whatever the purchasing company saw in the target business to pay the price it did.

If all goes well, goodwill becomes an oddity in a balance sheet. The value of the business grows and exceeds the accounting fiction. But if things go poorly, the business becomes less valuable and goodwill needs to be removed from the balance sheet. That’s the “impairment” bit and Stack Overflow’s goodwill has been removed from Prosus’ balance sheet to the tune of $1.459 billion. That’s right. The $1.8 billion purchase is now worth something in the neighborhood of $300 million.

| Year | 2022 | 2023 | 2024 | 2025 | 2026 | Total |

|---|---|---|---|---|---|---|

| Revenue | 54 | 94 | 98 | 115 | 129 | 490 |

| Revenue growth | - | 74% | 4% | 17% | 12% | 28%[1] |

| EBIT | (34) | (84) | (57) | (22) | 1 | (196) |

| Impairment | 246 | 560 | 372 | 0 | 281 | 1,459 |

(I gathered this data by looking at Prosus annual reports released after it purchased Stack Overflow. Other than revenue growth, these numbers are millions of dollars.)

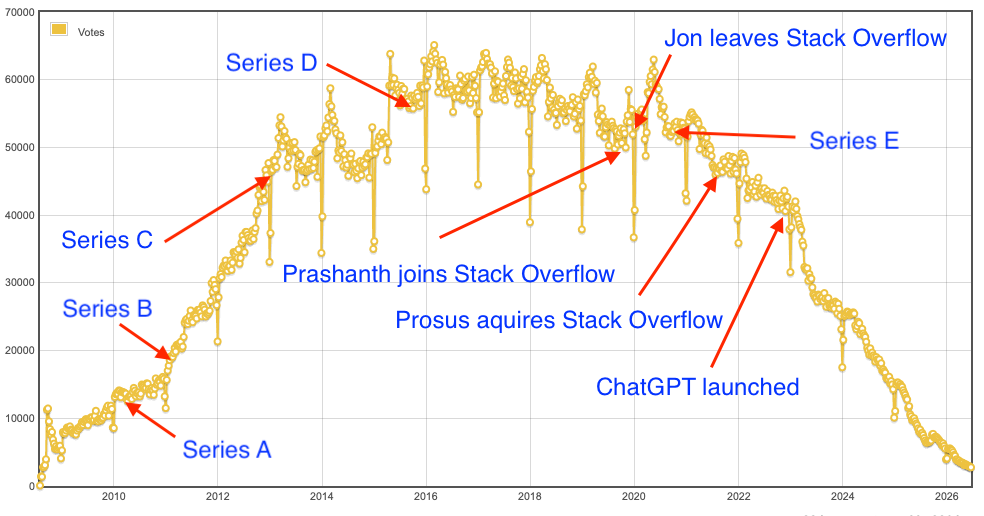

I was a bit surprised that revenue has grown by 28% annualized. Most of that gain came early on when Stack Overflow grew from $54 million in revenue to $94 million. That growth evaporated in fiscal year 2024 and I think I know why:

- Early in 2022, Stack Overflow began shutting down its Talent business. I’ve learned from insiders who left the company over the years that this line of business was profitable. But it didn’t fit with what the company thought was its core competency. I suspect the problem was that job listings wasn’t a high-growth, high-leverage business. In other words, it’s boring.

- Late in 2022, Stack Overflow migrated Teams to a new domain. I argued that this seemingly trivial change is “good way to kill Stack Overflow for Teams.”

- Early in 2023, Stack Overflow pushed all its chips into AI.

Management[2] ran hard and fast away from what had worked in the past toward the next big thing. The problem, of course, is nothing about Stack Overflow suggested that it would actually be good at making money from AI. The boring work of connecting developers with employers trying to hire developers (the business management abandoned in 2022) was a better fit than AI.

But miracle of miracles, it turns out Stack Overflow does have value for the AI economy! As the 2025 annual report puts it:

Stack Overflow achieved 17% revenue growth in local currency, reaching US$115m, with improved EBIT of -US$22m (from -US$57m in FY24) and cash flow breakeven. Success was driven by API partnerships, cost controls and new offerings like OverflowAPI for AI/LLM

providers. Challenges included GenAI adoption, user behaviour shifts and reduced marketing. Key milestones featured partnerships with Google Cloud, OpenAI, and others to advance GenAI developer tools.

Put in simpler terms, Large Language Models (LLMs) need huge amounts of data to train on. Stack Overflow has that data (especially for programming applications) and LLM providers are willing to pay Stack Overflow to get that data. What is that data? Well, it’s the collection of questions, answers, votes and comments contributed by users of Stack Overflow over the years. Technically it doesn’t belong to Stack Overflow, but rather contributors grant Stack Overflow a license to use it. (I’ve written about the issue in greater detail.)

Interestingly 2015 is the only year that Prosus didn’t record an impairment on its investment in Stack Overflow. The 2026 annual report is strangely quiet about Stack Overflow’s new business and Prosus resumed taking impairments to goodwill. Reading between the lines, I’m going guess the new business partnering with LLM providers isn’t going so well. Why not? Speculative, of course, but here’s my guess:

- The initial training stage for many LLM models is coming or has already come to an end. Stack Overflow data was certainly important to help models learn how to answer coding questions, but they are now getting trained from their own users.

- As my chart of voting over time on Stack Overflow shows, there’s not a whole lot of new Stack Overflow data anyway.

{kind=link}

So Prosus and Stack Overflow management had a goose that laid golden eggs and decided that wasn’t good enough.